While we look at daily vaccination numbers and listen to our leaders on how the road to recovery is within our grasp, the long term of the lockdown has undeniably impacted many businesses especially those who fall in the cracks like petty traders and micro SME’s. EMIR Research a think tank group had published numerous reports on loan moratoriums and just recently on Malaysia’s ‘Exit Strategy’ where it has called for extension to support the groups.

Just to update, a six month loan moratorium were given by the banks for those impacted by the pandemic when the country went into full lockdown during MCO 1.0, however the automatic extension ended in September and there has been calls for renewal for MCO 3.0. The think tank calls for more attention given to this and has some suggestions, the first objective is loan moratorium for all micro, small and medium enterprises (MSMEs), B40 as well as M40 households while targeted for other individuals for at least three (3) months or 50% loan payment reduction for six (6) months. However, the overwhelming uptake and benefit to the many in the backdrop of a potentially grave economic outlook suggest this to be extended to six months of automatic blanket loan moratorium.

The aim is to provide a safety net to those at risk due to the shutting down of economic activities and prolonged unemployment.

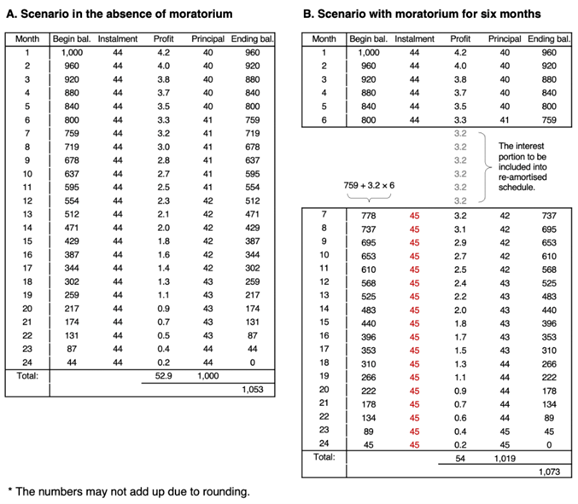

It is worth mentioning, a real moratorium that assists borrowers should have no room for the practice of charging borrowers an additional interest for the period of moratorium by re-amortising the loan payment schedule once the moratorium period is over. Under this practice, the total interest portion collection (profit) of which banks forego during the moratorium period is added to the beginning balance and thus result in a monthly instalment amount higher than the pre-moratorium one (Figure 1).

Figure 1. Illustrative example for the RM1000, two years loan at 5% p.a.

It has to be re-emphasised that the borrowers have not defaulted on their payments—the payments were merely postponed—and, provided the borrowers resume and finish all the payments according to the schedule, banks would not lose their real profits.

Although, banks would report some mere accounting losses (“day one” modification losses) due to re-evaluation of their outstanding loans. Under the International Financial Reporting Standards (IFRS 9), the banks have to show the fair value of the loans in their books based on the present value (PV) formula. Therefore, the fair value of the outstanding loans will reduce due to the newly extended period by the moratorium.

Also, banks would lose in terms of PV by postponing their collections to a later period. Receiving the repayment later than initially scheduled could affect the banks’ capital adequacy ratio whereby it has to increase its provisioning for possible loan default – which represents an opportunity cost to the bank. In 2019, loan loss coverage stood at 90%, and in 2020 this increased to 140%. However, this doesn’t in any way affect profits, as we shall see later.

Notwithstanding, the opportunity cost for banks under the current situation is limited in any case. That is to say, there may not be enough credit-worthy customers out there that would qualify under the banks’ stringent requirements for new loans, anyway. This would have boosted overall spending by way of the multiplier effect and circulation of cash in the economy (both businesses and households).

Instead, in the aftermath of the loan moratorium, banks lent out to purchase residential properties and passenger vehicles with the various tax incentives offered by the government. But the impact of such purchases has been limited—the loans which create the deposits are then not withdrawn for additional spending (and hence, the multiplier effect in terms of overall cash circulation).

Furthermore, it was in tandem with a steep decline in credit card loans which strongly points to a drop in overall spending activity during the pandemic, according to the June 2021 edition of the Malaysia Economic Monitor of the World Bank.

According to Bank Negara Governor, Nor Shamsiah Mohd Yunus, banks lent out RM206.2 billion in the fourth quarter of 2020, which exceeds the 2017-2019 quarterly average of RM196.7 billion. In the previous third quarter, the value of business loan disbursements stood lower at RM182.4bil. This indicates that banks’ lending activities, although affected by the loan moratorium but marginally.

Under the “Lockdown MCO 3.0 – Survive to restart package” published on May 29, we have explained when observing the income statements of major banks in Malaysia, that for some banks, net interest income does not seem to be a big profit contributor. Furthermore, lower interest income recorded has also been offset by lower interest expense – the costs of funds for the banks have also generally reduced in line with the lower interest rate environment.

Most importantly, we observe that once the moratorium has ended, based on the financial standing in Q1 2021, the ease of recovery for the banks was evident. If we examine net profits for Q1 2021 at the group level, we can observe examples of healthy profits from Maybank (RM 2.43 billion), Hong Leong Bank (RM 772 million), and RHB (RM 651 million). Keep in mind that these figures were still generated within the time where almost all borrowers took up the opt-in moratorium.

However, let’s now look at the other side of the coin as extensive focus on banks’ profits is duly uncalled for when many in the real economy straggle to protect the principle. It has full moral ground for the banking sector that has placed itself as a risk-free sector (including Islamic) to finally accept some reduced profits (not losses) and share the burden of the pandemic with the rakyat.

A relative reduction in profits to the banks attributable to the moratoriums is incomparable to the relative socio-economic harm to the people in the absence of a moratorium, especially during lockdowns.

The danger of massive loan defaults if the moratorium is not granted might be more real than we think.

Malaysia public indebtedness is at its historic high while the ability to service it is stretched unprecedentedly thin by the pandemic.

According to Bank Negara Malaysia (BNM), our household debt is at 93.3% as of December 2020, from the previous record high of 87.5% in June 2020. It’s second-highest in Asia after South Korea (but trails several high-income countries that exceed the 100% level, such as Australia, Switzerland, Denmark, Norway and Canada).

Even in the absence of the unprecedented pandemic crisis, this high level of indebtedness on the national scale should raise great concern.

The President of SME Association of Malaysia (SMEAM), Datuk Michael Kang, was reported to have projected a minimum of 40% of SMEs to shut down with the full-scale Movement Control Order (MCO), followed by many more job losses in the next few months. He stressed the urgent need for an automatic moratorium of at least six months to relieve the cash flow burdens of these businesses.

SMEAM Vice President Chin Chee Seong reportedly pointed out that at least 50,000 SMEs could go bust if MCO 3.0 is extended. And the extension is probable, if not necessary, given the unclear indicators of virus transmission control at present.

Chin was also reported to mention that according to the SMEAM’s survey, “only 8.6% of the SMEs said business is as usual, but the remaining 91.4% indicated that they will suffer losses from 25% to 100%”.

It’s best to note loan defaults only require disruption in cash flows and not have to wait for business closures.

Given that almost all businesses in Malaysia are SMEs (98.5% of all businesses) and provide a large chunk of employment, these figures indicate potentially devastating outcomes that would implicate the banks and not just these businesses and individuals.

In the fractional reserve and interest rate-based system, default is not a possibility but the certainty by the system design. The total extended loans cannot be repaid in aggregate simply because the interest payable does not exist in the money form. So, it is like a nationwide musical chair game—someone has to default. The question only is “who” and “when”?

To answer “who”, we know those are the B40s, low M40, and MSMEs. But, worrying enough, they are increasingly becoming the majority. According to the Economic Action Council (EAC) secretariat, more than 600,000 households from the middle 40% (M40) income group have slipped into the bottom 40% (B40) category.

While answering “when”, we would certainly like the answer to be distant and randomly distributed in time. The banking model works well as long as one person’s default is independent of other people defaulting.

However, the Covid-19 pandemic is the type of event that changes the probability of default for all borrowers simultaneously! And pushing them ruthlessly to pay loans now when their cash inflows are dwindling or halting will hasten the reckoning by this black swan event.

This will have drastic consequences not only for the banks but for the entire economy with the vicious cycles of more defaults, retrenchments and closures. The liquidity shortage will add to our already insurmountable mount of fighting the Covid-19 pandemic. As banks will be shaken to the core so will those who own a significant share of their profits – Khazanah, Employees Provident Fund (EPF), Tabung Haji to name just a few.

Is it not then far better to provide both parties, i.e., banks (lenders) and households and businesses (borrowers) with the “breathing space” now by extending the automatic moratorium for all?

However, some may still insist that not everybody needs an automatic loan moratorium.

Datuk Michael Kang was reported to mention that 90 per cent of SMEAM’s 15,000 members have taken advantage of the opt-in loan moratorium offered after the first six-month moratorium that ended on Sept 30, 2021. This indicates not only was the first automatic loan moratorium a welcome reprieve, but almost all felt the need to opt-in for the next round of moratorium – without which could have resulted in significant personal and business loans defaults.

The Finance Minister also reported that after the automatic loan moratorium ended in September 2020, 85% of borrowers resumed repayments.

Another way to look at this is that 85% of borrowers were able to resume payment precisely because loan moratoriums helped them keep their incomes by easing the cash flows of businesses. In the absence of moratorium, or focusing only on the 15% defaulters means the total number of defaulters may increase anywhere between 15% to 85%. The 15% figure means 15% of borrowers are in a bad enough position that not even moratoriums could help them survive. If anything, they need more assistance.

On the other note, 85% and 15% are all only the dry numbers. So could it be that the 85% have cash flow difficulties too? It’s just that the difference between 85% and 15% is the period (or inter-temporal capacity) over which the cash flow can last. That is, for the 85%, it’s only the case that their cash flow can stretch over a slightly longer period.

Has anyone asked what it would take for the 85% to resume their payments? Maybe they had to go to a pawn shop, or withdraw EPF savings, or go to loan sharks, or sell some of their assets or do other things detrimental to their wellbeing and human dignity. And did anyone even wonder how bad is the situation of those 15% who could not resume and what happened to them afterwards?

The blanket moratorium is not only direly needed but faster and easier to implement.

Extending the blanket moratorium will allow us to extend the safety net wide enough to capture all those in dire need, including the informal economic sector. And if this wide safety net captures few “free rides” (those who do not need moratorium but enjoy benefits of it), then let it be – we know those are very few compared to the majority who suffer.

We have seen how the previous moratoriums helped individuals and businesses stay afloat. These people were then able to resume repayments, and banks showed a healthy recovery thereafter. This win-win scenario is needed now more than ever.

Maybe for once, at least under the unprecedented circumstances threatening us all as a nation, the notorious value of profit as the be-all and end-all could give way to the universal value of life – the value of our life and lives of others.

Dr Rais Hussin, Dr Margarita Peredaryenko, Jason Loh & Ameen Kamal are part of the research team of EMIR Research, an independent think tank focused on strategic policy recommendations based on rigorous research.