About ten years after entering the global manufacturing sector’s consciousness, Industry 4.0 seems to have lost much of its novelty. Its principles, technologies, market drivers, and national government policies have become known quantities. Smart factories, the intelligent, hyper connected production plants that lie at the centre of Industry 4.0, have become detailed analysis and development objects.

Analysts predict robust future growth for smart factories and their contributions to global economic growth. Within the next five years, the study claims, intelligent factories will contribute up to $500 billion in value to the worldwide economy. Analysts now look to smart factories producing more goods and services at lower costs as the source of these gains. Manufacturers predict that by 2022, smart technologies will drive a sevenfold increase in annual efficiency gains. The report indicates that with smart technologies, some industries will nearly double operating profits and margins. Whether one believes that the oversized benefits these and other reports describe are believable, smart factories’ global manufacturing growth is a real trend, one is worth another look.

Big changes in the global manufacturing sector

Global manufacturing operations have undergone tumultuous times. Under globalisation, developing economies joined the global manufacturing value chain and fulfill the work at the lower

end of the supply chain, while first-tier manufacturing nations stay at the higher end. The system has proven to be vulnerable that in a case of a choking recession cutting off market demand due to unpredictable events like COVID-19, manufacturing verticals and employment will face a severe tumble.

Through all these difficulties, manufacturing activity remains a critical part of developing and technologically advanced economies. Manufacturing provides a path to better incomes and living standards. In developed economies, manufacturing still provides a vital source of competition and innovation. It is a significant source of exports, research and development, and productivity growth. A good example is Germany, whose 47% of GDP is made up of manufacturing and its 27% of exports to the UK are vehicles.

The global manufacturing sector changes, bringing challenges and opportunities to manufacturing businesses of national and regional economies. However, business leaders or policymakers should assume future success based on old habits. So, what can one say about the future?

Manufacturing in the future

As nations mature economically and technologically, manufacturing is part of essential shifts in national societies. In a 2018 report, the McKinsey Global Institute clearly describes how manufacturing adds to the global economy.

Some of its key ideas include:

Manufacturing’s changing role. In advanced economies, manufacturing drives productivity, innovation, and trade more than employment and economic growth. Manufacturing in these countries has also started to use more services rather than relying heavily on making and selling their products.

Currently, manufacturing adds 14 percent to global employment and 16 percent to global GDP. However, the sector’s relative size in a national economy varies with its stage of development. In industrialised economies, they drive manufacturing output and employment growth. However, when manufacturing’s GDP segment peaks at 20 to 35 percent; it falls in an upside-down U pattern. As wages rise, consumers will spend more money on services. The service sector’s growth

accelerates, making it more important than the manufacturing industry as a source of improved GDP and employment.

Renew understanding of manufacturing’s role. The manufacturing sector is also changing in other ways. Traditionally, manufacturing and services have been viewed as different sectors. This view is outdated. From advertising to logistics, services add up to a more significant part of manufacturing activity. In a year, every U.S. dollar of manufacturing output includes services worth 19 cents. More than half of the employees have moved to service industries in some high-tech and engineering industries, such as office support staff and R&D engineers.

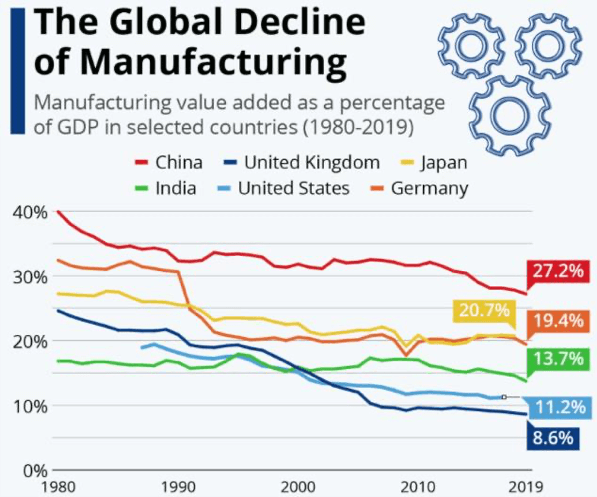

Figure 1: The Global Decline of Manufacturing

(Source: United Nations and World bank https://www.statista.com)

In the future, however, the manufacturing share of employment will continue to decrease. The drivers for such trends include long-term productivity improvements, faster service growth, and a global competition faced. These powerful forces push developed economies toward specialisation in jobs that require increased levels of work skills.

Manufacturing is not monolithic

Each national manufacturing sector is unique. In some nations, work in specific industries is more labour- or knowledge-intensive. Some economies rely more heavily on transportation, while for others, being close to customers is a critical part of manufacturing growth. The authors cite five general manufacturing segments in the recent McKinsey report and then measure how production factors determine where manufacturers will build up factories as part of their Go-to-market strategies.

The largest segment by output (measured as annual gross value added) includes chemicals, autos, and pharmaceuticals. These industries rely heavily on R&D activity, global innovation, and the need to stay close to their customers. Next in size is regional processing. This segment includes printing and food & beverages. These labor-intensive trade goods are the smallest segment, with only 7% of worldwide value-added. Hence, given the significant dynamics, the only way to understand global economic activity is to make a detailed analysis of each nation’s manufacturing sector.

A new phase of uncertainty and active change

Global manufacturers might have significant new business opportunities. However, they must operate in a more and more uncertain economic environment. Questions like ‘Who will be our customers?’ and ‘What do they want, and what will labour and other resources cost in the next ten years?’ will be constantly asked by the manufacturers themselves.

Expect the emergence of a new global consumer class and that most consumption will occur in developing nations. This situation creates lucrative opportunities for manufacturers in emerging markets. In developed economies, the demand for mass-produced products is shrinking. In contrast, customers want a wider variety of products, more personalised designs, and a specific after-sales service to the individuals’ preferences. Based on such needs, a wide variety of new materials and

processes, from 3-D printing to advanced robotics, indicate a greater demand and drive more productivity gains.

These opportunities appear in a challenging economic environment though. In lower-cost labour markets, wages are rising quickly. Resource prices are volatile, and a coming shortage of high-skilled talent creates more financial risk than existed before the Great Recession in 2008-9. With the COVID crisis, more manufacturers are seriously considering mitigating the risk with technology-based transformation in both their operations and business models.

Policymakers in developing new approaches

To compete in this dynamic age, manufacturing companies must:

• Understand customers more. Companies must realise specific emerging markets and the needs of their existing customers.

• Develop agile strategies and production processes. Decision-making speed is as essential as rapid-fire production methods. Customers are changing their minds about what they want to buy. And, they will support manufacturers who have what they want, when they want it.

• Be willing to make big bets on long-range opportunities. Growth via better efficiency is one of many routes to manufacturing success. Finding and acting on new business opportunities is another. Manufacturers must be willing and ready to make bets on long-term prospects. All these are absolutely high-pressure decisions – manufacturers must be willing to enter new markets or switch to new methods and models to run their business.

• Approach production and marketing strategies in a subtler way. In the past 30 years, market activity shows that labour-intensive industries’ behaviour almost always resembles low wages. Most of these business opportunities are drying up. More nuanced manufacturing strategies must balance factors such as access to high-skilled employees or lower-cost transportation.

• Policymakers need to step in and help manufacturers compete globally. They should:

o Have a thorough knowledge of their manufacturing sector. They must set policy with a detailed understanding of the many industry segments that make a national or regional economy.

o Make education and skills development top priorities. Policymakers should understand that supporting critical enablers is the best way to support ongoing growth, exports, and innovation. Two necessary preferences for governments and businesses include education and skills development.

Policymakers should help manufacturers build their R&D capabilities by upgrading product design and data analytics knowledge and skills. Companies will need computer-savvy production operators and responsive managers who can run worldwide supply chains. Improving public education— especially mathematics and analytical skills—is another must-have capability. Policymakers must collaborate with industrial and educational institutions so that skills learned in school fit the needs of employers.

(In part 2 we shall discuss on Potential Manufacturing Pitfalls)

Written by Colin Koh, Senior Business Development Manager, Industry 4.0 Consultant of LKH Precicon in Singapore. He is a technology evangelist, digital transformation specialist, and highly respected figure in the ASEAN business community. Colin previously served as the President of the Singapore Industrial Automation Association (SIAA), is a certified IoT specialist, and an MIT Sloan School of Management Executive program in Artificial Intelligence and IoT. Colin currently provides

mentorship and advisory to companies implementing digital transformation towards Industry 4.0.