By Deloitte Malaysia’s Global Employer Services Executive Director, Chee Ying Cheng and Associate Director, Lee Lai Kuen.

Since 2004, foreign income brought back to Malaysia by an individual enjoys an income tax exemption. However, this will no longer be the case beginning 1 January 2022 for Malaysian tax residents. This tax exemption has been removed to demonstrate the country’s commitment to compliance with international best practices. For non-tax resident individuals, they will still continue to enjoy the exemption.

Due to this change, law-abiding individuals who wish to remit their monies into Malaysia will now need to be more prepared to cope with various issues and challenges stemming from this rule. Just to name a few:

- Taxable vs non-taxable

As not all monies remitted into Malaysia are taxable, an individual would need to ascertain if the remittance will be subject to tax under this new rule. One would need to determine if it is a foreign-sourced income (FSI) as opposed to, say foreign-sourced capital. The former (i.e. FSI) is taxable while the latter is not.

- Segregate the “mixed”

Taxpayers may have accumulated monies overseas over a long period of time from various sources. For example, a mixture of foreign income, capital, or even Malaysian source income is deposited into foreign bank accounts for children’s education, investment purposes, etc. As such, one has to have comprehensive records from the very beginning to clearly identify the nature of the “mixed” funds in one’s portfolio to ensure that they are not under, or over-stating FSI for tax purposes.

- Gross or Net

Generally speaking, the Income Tax Act 1967 (“the Act”) states that income (i.e. business, employment, interest, royalties, and pension) is a tax chargeable on a gross basis. However, the Act is silent on whether the “income received in Malaysia from outside Malaysia” would be subject to tax on a gross or net amount basis. Based on the reading of the Act, the remittance of FSI would be subject to tax on a gross basis, unless stated otherwise.

The adoption of a gross basis for the taxation of FSI would make it difficult for individual taxpayers to accurately determine the gross amount to be included in their tax returns. As most countries tax personal income on scale rates, this would be an added layer of difficulty to the taxpayers in determining the gross amount to tax in Malaysia.

- The “petty” challenge

Is remittance of FSI merely limited to the physical transfer of funds to Malaysia? Or will the following scenarios also be construed as a remittance?

- Using a foreign credit card for expenditure used or enjoyed in Malaysia

- Use of foreign income to pay off a debt created in Malaysia (i.e. a debt in respect of something which is used or enjoyed in Malaysia such as purchase of a real property)

- Transfer of money to someone else who then uses the money to buy goods and services in Malaysia

- Personal items (e.g. clothing, footwear, jewelry, watches) purchased overseas with FSI and brought to Malaysia for personal use

If the above is to be regarded as “FSI received in Malaysia”, then both the individual taxpayer and the tax authorities will have an arduous, if not impossible, a task in tracking each transaction. The additional tax revenue to be collected would not be compensated by the need for additional and cumbersome administrative processes for all parties involved.

What can we do – some suggestions

- Setting a floor amount

The Government may consider adopting a “de-minimis” rule for individuals, where the new rules kick-in only when the amount of foreign income received into the country exceeds RM50,000 annually.

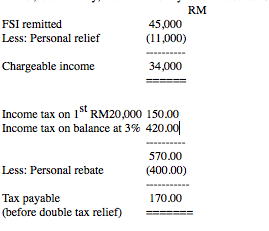

Assuming a married resident individual (with a child) with no Malaysia sourced income remits FSI of RM45,000 annually, their tax liability is estimated as follows:

Based on the above example, the additional tax arising from the remittance of RM45,000 per annum is a mere RM170. This amount may be reduced to zero after taking into account the double tax relief (foreign tax credit equivalent).

Since the potential additional (if any) tax revenue is expected to be minimal at this level of remittance, the proposed de minimis amount shall alleviate the administrative tracking and collection challenges faced by the tax authorities and the middle-income group of individual taxpayers.

- Start on a clean slate

Another often-asked question is whether income earned prior to the implementation of this rule be taxed when remitted into Malaysia with effect from year 2022.

A simple illustration is as follows:

- An individual has been working overseas for many years and returns to Malaysia on 1 January 2022.

- They will establish Malaysia tax residency earliest by 1 July 2022.

Are the funds taxable in year 2022 since it was remitted into Malaysia in the year the FSI exemption was removed, despite being income earned when the FSI exemption was still valid?

Perhaps we can look to the UK for guidance as their taxation system encompasses the taxation on the remittance of foreign source income.

A UK tax resident whose permanent home is outside the UK will be taxed on foreign income that are paid in or remitted to the UK, subject to certain restrictions. However, one would not be taxed on remittance of overseas income earned before one becomes a UK tax resident.

Malaysia may consider adopting a similar approach i.e., taxing an individual on FSI earned only after they become a Malaysian tax resident, and not before. Therefore, based on the illustration above, FSI earned before 1 July 2022 and remitted should not be taxed in Malaysia, while FSI earned after 1 July 2022 will be taxed, if brought back to Malaysia.

This will allow a taxpayer to start on a clean slate and not need to trace the FSI accumulated over the years.

- Adopt an equitable treatment between local and foreign source income

Currently, dividends from local companies and interests from local banks received by individuals in Malaysia are exempted from tax. However, the implementation of the new rules will tax the remittance of foreign dividends and interests into Malaysia by a tax resident. Therefore, the individual who receives and remits any foreign dividends and interests would now be tax disadvantaged as compared to one who derives the same income locally. This does not seem to be aligned to Budget 2022’s focus of building equitable tax treatment in line with international regulations.

To achieve some form of equality, the Government may look to countries such as Singapore, Thailand, Indonesia, and Philippines where FSI is taxable but foreign dividend is exempted from tax, subject to conditions.

Tax filing just became more difficult

The Self-Assessment System (SAS) was implemented (year 2004 for individuals and 2001 for companies) around the same time when the FSI exemption was introduced in year 2004 for individual taxpayers, thus simplifying tax matters for individual taxpayers.

Under the SAS, a taxpayer is responsible for computing one’s own chargeable income and tax payable, as well as making payment of any balance of tax due. The amount of tax payable for the year must be self-computed, and the tax return is deemed to be a notice of assessment upon submission.

Since FSI which have already suffered foreign tax is eligible for a double tax relief claim against Malaysian tax, an individual taxpayer would need to determine the amount of eligible relief. At time of writing, the Government is adopting a broad-based approach in taxing foreign income, hence the calculation and claiming of double tax relief in the Malaysian tax return may be a complex process.

The analysis of types of income subject to tax and double tax relief calculation are not common steps in the tax filing process and common individual taxpayer are not adequately equipped for such steps. Compounded that we are now under SAS where hefty penalties will be imposed on the taxpayer in the event of a tax audit by the tax authorities, wherein there are errors/incorrect reporting in the tax return.

While we understand the need for the Government to implement an equitable yet competitive taxation system, it is hoped that the Government can consider the suggestions and alleviate some of the pain points for individual taxpayers with rules coming in effect 1 January 2022.