The economic outlook for the United States for 2023 has deteriorated under the weight of high inflation rates and rapid monetary tightening.

Falling consumer and business confidence, softening consumption and investment, and geopolitics-induced energy shocks are likely to tip the economy into recession around the turn of the year.

However, the recession is projected to be short and mild, amid a strong labor market and relatively heathy consumer and business balance sheets.

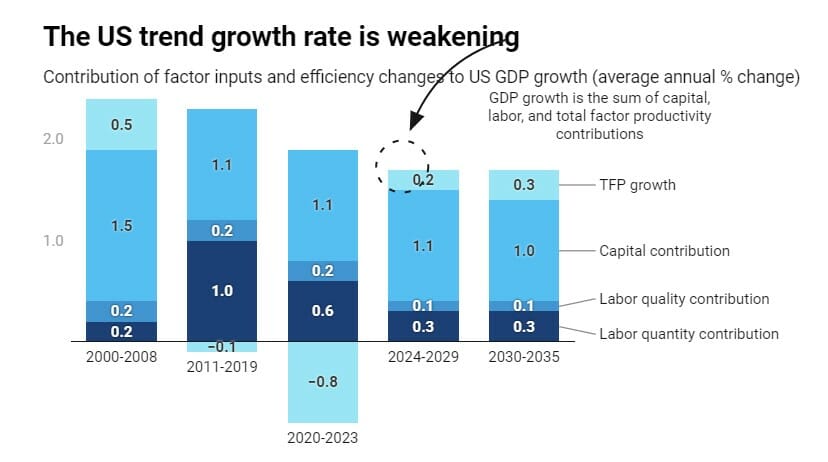

Beyond 2024, the US economy is likely to return to its slowing trend growth rate trajectory. Key risks around the longer-term US outlook are related to geopolitical frictions, environmental challenges, labour markets, and inflation, The Conference Board opined.

Insights for What’s Ahead

We expect the US economy to go into a recession as we enter 2023. Following a large drop in US gross GDP in 2020 due to the impact of the COVID-19 pandemic, the US economy experienced rapid growth for much of 2021. However, in 2022 this growth momentum began to sputter.

We expect inflation to remain above pre-pandemic trends for several years, if not longer. The US economy is currently grappling with a wave of high inflation driven by a confluence of supply and demand factors that we do not expect to resolve quickly.

We do not expect interest rates to fall until 2024 or later. As a function of inflation, the Federal Reserve has rapidly tightened monetary policy and will continue to raise rates into early 2023.

Following our expectation of near-zero growth in 2023, we expect US real GDP growth to recover in 2024. However, over the next decade, growth will be somewhat muted relative to pre-pandemic trends.

Disruptions brought about from the pandemic will have lasting effects on the drivers of US growth ahead and there will be smaller contributions from labor, reflecting an aging demographic. Nonetheless, acceleration of digital transformation resulting from the pandemic and current investments in infrastructure are likely to result in elevated total factor productivity (TFP) growth over the next decade.