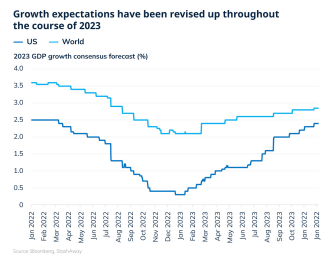

A gradual slowdown in growth

To answer the Goldilocks question, let’s first take a look back to 2023. The US economy has been much more durable to the impact of rate hikes than expected, with GDP growth forecasts ending the year back where they started in early 2022. This strength has been largely due to a stronger-than-expected US employment – the result of COVID-related shifts in the labour market.

Our view is that a more substantial slowdown in US growth will eventually pan out in 2024 as high interest rates take their toll. But given these dynamics in the jobs market, it will likely be very gradual.

Inflation may remain sticky

That’s why we believe the outlook for inflation has bigger implications for markets. Here, the path for inflation to return to the US Federal Reserve’s (the Fed) 2% target could be a bumpy one. In particular, we see supply-side pressures from the labour market and oil prices as key upside risks to inflation (read on for our full analysis).

And because supply-side drivers of inflation tend to be more persistent – and could risk keeping us in a stagflationary environment for longer – this suggests that investors should continue to err on the side of caution.

What does that mean for your investments?

On an asset class level, given that we’re still not out of the stagflation regime, our investment framework, ERAA®, continues to place an overweight on shorter-duration bonds, like US Treasury bills, and defensive assets like gold.

Once the coast is clear on inflation and the economic data show a clearer shift toward recession (or in the best-case scenario, a soft landing in “good times”), that’s when ERAA® can lengthen duration for our fixed income holdings.

Equities also appear to be pricing the perfect scenario of a soft landing, and have been closely mirroring returns of the bond market – meaning a more cautious stance going into the new year is warranted. Taking a longer-term view however, we see attractive opportunities in selected structural themes (more on that in Part 2 of our 2024 H1 Outlook series in January).

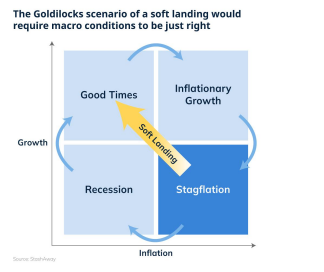

What does ERAA® say about the odds of a soft landing?

One way to understand why soft landings are so rare is to look through the lens of our ERAA® framework, which is based on the typical flow of the economic cycle as it expands and contracts.

Since December 2022, ERAA® has signalled that we’re in stagflation, where growth is stalling and inflation is still high. A soft landing would mean a swift move in the economy from stagflation back into “good times” – skipping over recession completely. For this to happen, that would require a lot of things to go right.

Consistent with our ERAA® framework, investor concerns cycle between growth and inflation, and this manifests itself in how asset classes behave. Put simply, when investors are worried about growth, equities suffer; when they’re worried about inflation, bonds suffer.

Take COVID: as investors were concerned about the health of the global economy (as well as their own health!), equities plunged and bonds rallied.

And even if the economy does fall into a recession next year, we don’t necessarily consider such an outcome to be a bad thing, from an investment perspective. That’s because the rate hikes of the past year or so have left room for the Fed to reduce rates if needed – which would be supportive for both stock and bond prices.

Stagflation, however, is a trickier regime for investors to navigate, as they need to worry about both growth and inflation at the same time. That’s why we argue that the biggest risk for markets in 2024 is not that the economy moves into a recession, but that it stays in stagflation.

Read on for a deeper dive into what could keep the economy in stagflation, or jump over to our perspective on returns.

Sticky inflation could lead to a bumpier landing

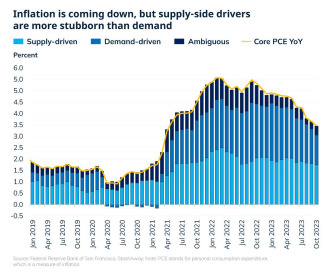

Understanding persistent supply-side inflation is key to the path ahead. That’s because this type of price pressure tends to be harder to shake out of the system – meaning that a further slowdown in growth wouldn’t be able to bring down inflation.

Indeed, the data suggest we should remain cautious. A study by the San Francisco Fed shows that most of the disinflation in recent months has been driven by a slowdown in the demand-side (shown by the navy blue bars in the chart below). Meanwhile, supply-side inflation (the light blue bars) has stayed sticky.

StashAway sees two major forces driving this stickiness in supply-side inflation:

1. A strong US labour market tied to a structural shortfall of workers post pandemic (see our 2023 H2 outlook for a deeper dive into this topic). 2. Persistent tightness in global oil supply. Crude oil prices have been relatively well supported in a US$70-90 range since 2021 amid OPEC production cuts and a significant drawdown in US oil reserves. This compares with a $40-70 range in the late 2010s, when the world faced a different problem – an oil glut.

For oil, geopolitics could further complicate the picture. Historically, most regional conflicts – like what’s happening now in Eastern Europe and the Middle East – have only resulted in short-term price fluctuations.

But today the impact of geopolitics on inflation is magnified given that oil supply is already tight and core inflation is still elevated. That means any shocks to commodity prices could result in more turbulence for the economy and markets.

Look back to the 1990s for clues on the future

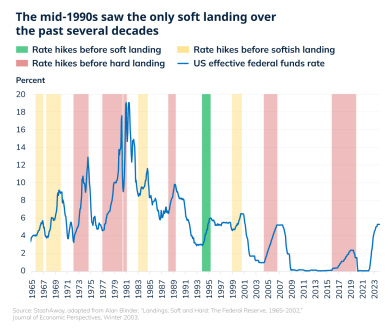

If we take a look back on history, soft landings have been hard to pull off.

Take the mid-1990s, which was one of the rare times when the Fed was able to achieve such an outcome. In 1994-95, the US central bank gradually raised the fed funds rate from 3% to 6%, then lowered it to 5.25% over the following year as the economy cooled. At the same time, GDP growth averaged more than 3%, unemployment actually declined, and inflation was stable.

But the 1990s were also characterised by economic expansion and stability, with no major price shocks (like the oil price spikes of the 1970s-80s, for example). In addition, during the late 1990s the US experienced a major pick-up in productivity that was attributed to technological innovation – which helped sustain economic growth without stoking inflationary pressures.